Title, Escrow & Appraisal Fees + Closing Costs + Home Warranty

Contract — Page 5: Fees, Closing Cost & Home Warranty

Seller closing cost contributions, ACHOSA home warranty, and cash deal handling.

Section 7.D — CLOSING FEES: Seller’s contribution toward Buyer’s closing costs. These costs include lender fees, title and escrow fees, and the Buyer’s recurring or non-recurring closing expenses.

Seller Contribution — Investors max 2%. Owner-occupier, aim for 2.5% – 3.5%.

Get in touch with the Lender to know how much is needed for closing costs. Our partnered lenders at ZHL & Note Mortgage are top-notch in communication.

If you write “3%” and counters push the price down by $20k, the seller’s contribution drops proportionally. Writing a fixed dollar amount locks in the contribution. Investor cap is 2% by most loan programs — owner-occupier rules are more flexible.

Section 7.E — HOME PROTECTION PLAN: Coverage for the Buyer after Close of Escrow.

SG Warranty Partner — ACHOSA. We have a great relationship with Lisa Waldeck. $825 covers the Prime Plus plan.

If the home didn’t have major issues on the inspection, the warranty will most likely cover post-close items at the warranty company’s policy limit. Set the expectation: warranty is a safety net, not a free repair plan.

ACHOSA’s choose-your-own-vendor feature is huge — most warranties force you into a specific contractor pool, which means slow service and lower quality. ACHOSA gives the homeowner control.

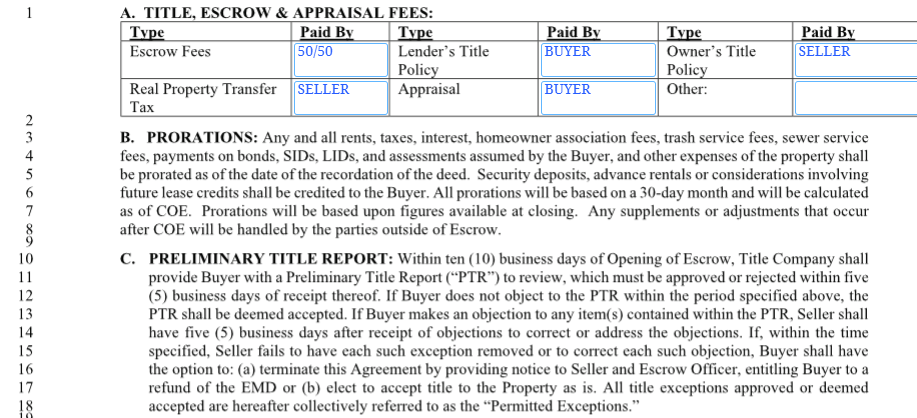

Section 8 — Title, Escrow & Appraisal Fees / Preliminary Title Report: Who pays for the Owner’s Title Policy, Lender’s Title Policy, Escrow Fee, and Appraisal.

A cash buyer CAN pay for an appraisal if they wish — but it’s optional. The Preliminary Title Report should be reviewed by the Buyer for any liens, easements, or restrictions.

Lender’s Title Policy and Appraisal both exist for the lender’s protection. No loan = no lender = neither applies. (A cash buyer can still optionally pay for appraisal for due diligence.)