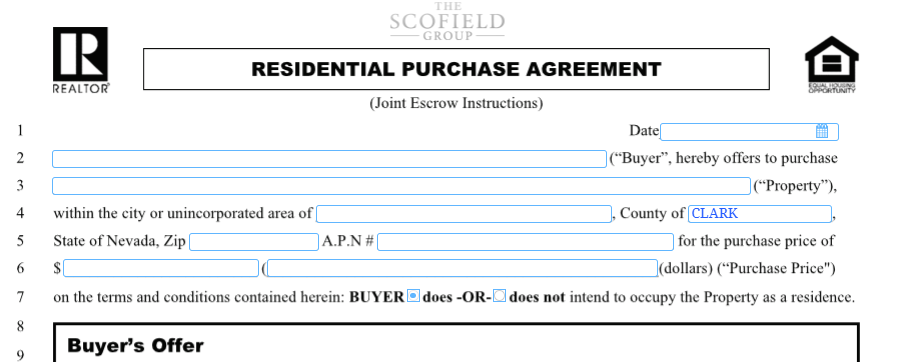

Financial Terms & EMD — Buyer, Property, Loan Type

Contract — Page 1: Buyer, Property, Offer & Loan Details

Buyer info, intent to occupy, EMD, loan type, purchase price reconciliation.

Occupancy status drives loan type eligibility (owner-occupied vs investor pricing), homeowner’s insurance vs landlord policy, and property tax handling (homestead exemption). Get this wrong and the file gets kicked back during underwriting.

LINE 12 — EMD Rule of Thumb Under FHA limit (2026 = $561k): $3k max, start at $1-2k. $561k-$832k: $3k-$5k. Above $832k: $10k+.

LINE 13 EMD is always to be wired. Send the Wire Fraud Notice Disclosure with the RPA — every time.

LINE 14 Allow your buyer two (2) business days to wire the earnest money.

LINE 15 Escrow Holder — always.

The EMD dollar amount is 100% negotiable. Use the rule of thumb as a starting point, not a ceiling.

Earnest money signals buyer commitment to the seller. Too small reads as a weak offer; too big puts the buyer’s cash at unnecessary risk. Wire fraud is the #1 real estate crime — the disclosure puts verification obligation on the buyer in writing.

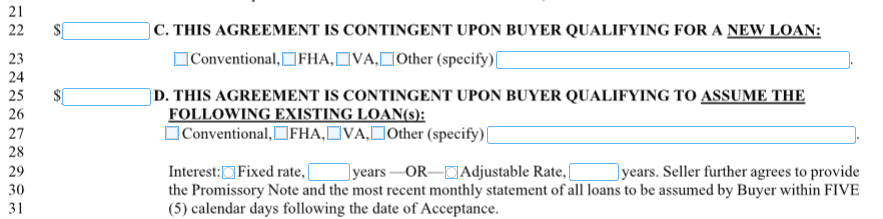

LINE 22 — Loan Amount FHA = 96.5% of purchase. Conventional = whatever buyer puts down (usually 10-20% down → 80-90% loan). VA = 100% = full purchase price.

LINE 23 — Loan Type Choose the appropriate Loan Type. If the buyer has to change in escrow, it must be mutually agreed upon with the seller.

If a buyer switches loan type mid-escrow (e.g., conventional to FHA), the seller is suddenly waiting on appraisal and contingency timelines they never agreed to. Without mutual agreement, the seller can cancel and keep EMD.

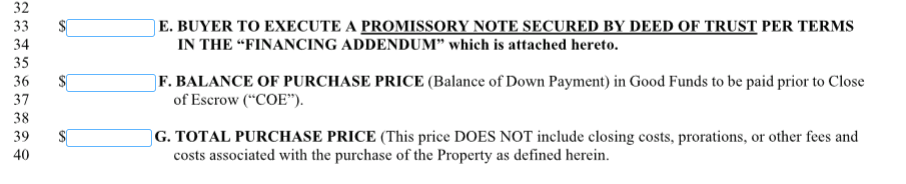

LINE 36 — Purchase Price Reconciliation If VA, then (−EMD$$). Line 39 = Purchase Price.

The math has to reconcile across EMD, loan amount, and balance to equal the purchase price. If lines don’t add up, Title bounces the contract back and you lose days in escrow waiting for an amendment.