Commission & Contingencies — Loan, Appraisal, Cash Purchase, Sale of Other Property

Contract — Page 2: Commission & Contingencies

Buyer Agent Commission, Loan Application, Appraisal Contingency, Loan Contingency, Cash Purchase, and Contingent on Sale.

Section 2 — BUYER REPRESENTATIVE/BUYER BROKER COMPENSATION: At close of escrow, Seller pays Buyer’s Broker the commission shown here.

You may charge a % OR a Flat Fee (land deals or specific negotiated terms). Do NOT have both filled in.

If you don’t have a commission on here AND you don’t have a BBA with an amount agreed prior — you will NOT be paid. Choose the amount, but be mindful of your NET and discuss the full terms with your Buyer.

The commission you charge on the RPA cannot exceed the Pre-Showing Buyer Brokerage Agreement you signed earlier. If you signed at 2.5% and write 3% in the RPA, you’ve created a legal conflict and may not get paid.

Section 3.A — NEW LOAN APPLICATION: Within the specified business days following Acceptance, Buyer agrees to (1) submit a completed loan application AND (2) furnish a pre-approval letter.

Line 9 — If CASH: enter N/A. If Loan: enter 1 (or INCL) as Pre-approved to offer attached.

If Buyer fails to complete any of these within the timeframe, Seller can terminate. Both parties agree to cancel escrow and return EMD to Buyer. Buyer must use best efforts to obtain financing under the terms outlined.

Listing agents look at the loan application date as a signal of buyer seriousness. A short window (1 day) shows the buyer is committed. Padding it past 5 days reads as a buyer who’s still shopping — some sellers will pass.

Section 4 — SALE OF OTHER PROPERTY: Is this offer contingent on the Buyer selling another home?

If your buyer needs to sell a home, that home most likely needs to be IN ESCROW for the offer to be accepted. Include the Contingent Upon Sale Addendum with the offer.

Sellers almost never accept a contingent-on-sale offer unless the contingent home is already in escrow. Get them in escrow first, then write the new offer — otherwise you’re wasting your buyer’s hope.

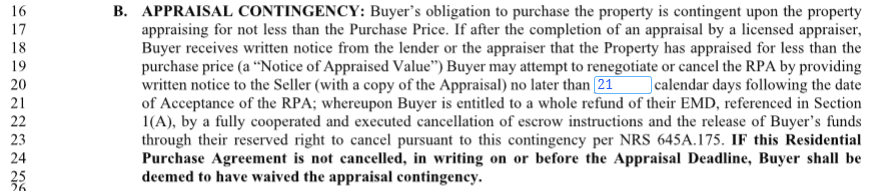

Section 3.B — APPRAISAL CONTINGENCY: Buyer’s obligation is contingent upon the property appraising for not less than the Purchase Price.

Line 20 — Appraisal Contingency Days. Suggested: 21 days (discuss with lender). Place expiration in Google Calendar 2 days prior AND day-of.

ZHL provides a FREE appraisal which saves the client $500-$1000. Appraisals are paid at the beginning of escrow — verify the client has funds for appraisal AND home inspection ($800-$1000 on average).

21 days gives ZHL and most lenders the runway to order, complete, and deliver the appraisal. Too short and a delayed appraisal forces you into a waive-or-cancel decision your buyer isn’t ready for.

Section 3.D — CASH PURCHASE: Within the specified business days, Buyer provides written evidence from a bona fide financial institution of sufficient cash to complete the purchase.

Line 36 — Proof of Funds. If LOAN: N/A. If CASH: enter 1 (or INCL) as POF will be attached with the offer.

Cash offers without POF look untrustworthy to listing agents. POF attached at offer eliminates the back-and-forth that usually kills cash deals during the response window.

Section 3.C — LOAN CONTINGENCY: Buyer’s obligation is contingent on obtaining the loan in Section 1.C or 1.D. Buyer must remove the loan contingency in writing, attempt to renegotiate, or cancel the RPA.

Line 30 — Loan Contingency Days. Suggested: 25 days. Place expiration in Google Calendar 2 days prior + day-of.

Lines 33-34 — FINAL Approval. If they do NOT have FINAL approval (not conditional — FINAL APPROVAL) by this date, get an extension prior. Otherwise they must waive in writing or cancel.

Condos require a Condo Cert Approval if not on the approved list (occupancy mix and litigation).

Place this in Additional Terms on Page 9 of 11: “Buyer and Seller agree that if at any time Lender cannot obtain (if FHA put FHA in front) Condo Cert Questionnaire Approval, then Buyers Earnest Money to be refunded back to the buyer.”

Conditional approval is not enough — underwriting can still deny. Conventional lenders also require the entire HOA to be approved for lending (occupancy mix, litigation, reserves). Without the cert language, your buyer is exposed: if the condo fails approval, they lose EMD.